Does Macrs use salvage value

By James Craig

When using MACRS, an asset does not have any salvage value. This is because the asset is always depreciated down to zero as the sum of the depreciation rates for each category always adds up to 100%. … For example, depreciate an asset classified under 3-Year MACRS for 4 years.

Does MACRS ignore salvage value?

This system determines the depreciable lifetime of your property and offers its own set of depreciation methods. Under MACRS, you simply ignore salvage value.

What qualifies as MACRS property?

The modified accelerated cost recovery system (MACRS) is the proper depreciation method for most assets. … Depreciation using MACRS can be applied to assets such as computer equipment, office furniture, automobiles, fences, farm buildings, racehorses, and so on.

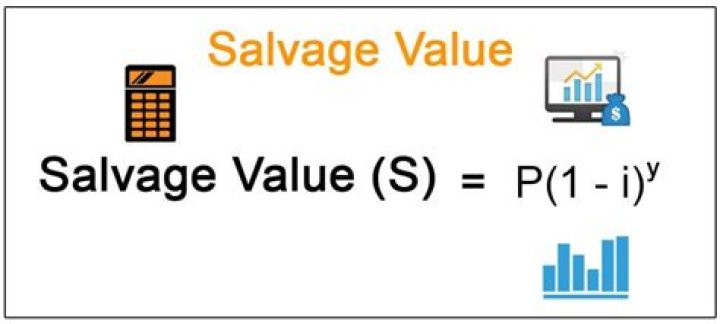

How do you calculate salvage value from MACRS depreciation?

Straight line depreciation = (Original cost – salvage) / useful life in years. MACRS depreciation = Original cost x MACRS percentage, based on MACRS tax life and specific year for depreciation.How does MACRS depreciation work?

The MACRS depreciation method allows greater accelerated depreciation over the life of the asset. This means that the business can take larger tax deductions in the initial years and deduct less in later years of the asset’s life.

Is MACRS straight line depreciation?

MACRS formula depreciation uses either a declining balance formula or a straight-line formula. In the MACRS straight-line method, LN calculates a new applicable percentage of depreciation in each year of the asset’s life. … In subsequent years, LN divides the depreciation amount evenly across each period in the year.

What is MACRS 5 year property?

5-year property. 5 years. Automobiles, taxis, buses, trucks, computers and peripheral equipment, office equipment, any property used in research and experimentation, breeding cattle and dairy cattle, appliances & etc.

What is the difference between MACRS and ACRS?

The main difference between ACRS and MACRS is that the latter method uses longer recovery periods and thus reduces the annual depreciation deductions granted for residential and non-residential real estate. … In March 2004, temporary and proposed changes to MACRS were published by the IRS.What are MACRS depreciation conventions?

MACRS convention determines the number of months for which you can claim depreciation during a partial year, either when you first placed the asset in service or when you disposed of it.

Is 200 db the same as MACRS?Reports will show the depreciation method allowed under MACRS (200DB, 150DB, S/L) that is being used to calculate the current depreciation for an asset, rather than displaying MACRS. This is the same as how the method is reported, per IRS instructions, on Form 4562.

Article first time published onHow do you use the MACRS method?

- Determine your basis, namely the original value of that asset.

- Determine your property’s class. …

- Determine your depreciation method. …

- Choose your MACRS depreciation convention, namely the time you first started using that asset. …

- Determine your percentage.

Can I depreciate my residential solar panels?

Solar is generally depreciated over a 5-year depreciation schedule, which means the cost basis of the equipment can be depreciated (similar to expensing or writing off costs) completely over 5 years. … Depreciation for residential solar arrays is generally not allowed unless it is considered a business expense.

Does MACRS tax depreciation?

The Modified Accelerated Cost Recovery System (MACRS) is the current tax depreciation system in the United States. Under this system, the capitalized cost (basis) of tangible property is recovered over a specified life by annual deductions for depreciation.

How do you calculate MACRS depreciation on rental property?

How do you calculate depreciation? If you own a rental property for an entire calendar year, calculating depreciation is straightforward. For residential properties, take your cost basis (or adjusted cost basis, if applicable) and divide it by 27.5.

How do you use MACRS depreciation schedule?

When calculating depreciation expense for MACRS, always use the original purchase price of the asset as the depreciable base for each period. Note that you depreciate each category for one year longer than its classification period. For example, depreciate an asset classified under 3-Year MACRS for 4 years.

Who can use Macrs depreciation?

Tractors, racehorses (over 2 years old), qualified rent-to-own properties, etc. Automobiles, office machinery, computers, etc. Office furniture, agricultural machinery, railroad tracks, etc. Water transportation equipment, single-purpose agricultural structure, tree or vine-bearing fruits, etc.

What code section is Macrs depreciation?

Depreciation is the amount you can deduct annually to recover the cost or other basis of business property. This must be for property with a useful life of more than one year.

What year did Macrs depreciation start?

The Modified Accelerated Cost Recovery System (MACRS) is a form of accelerated depreciation enacted by the US Congress in 1981 and 1986. MACRS remains remains in place, today, as the centerpiece of the US Internal Revenue Service Tax Code depreciation of business assets.

What is the difference between straight line and MACRS?

On a graph, the asset’s value over time would appear as a straight line sloping downward, hence the name. In contrast, the default MACRS depreciation method gives you a bigger tax deduction in the early years, while the asset is still new, and a smaller deduction towards the end of the asset’s useful life.

What MACRS Convention applies to the assets?

Every MACRS asset placed in service in the current tax year is subject to either a half-year, mid-month, or mid-quarter convention. These conventions apply only to assets with a method of “M,” “ME,” “MT,” “MSL” or “ADS.”

Why is accelerated depreciation MACRS useful for a firm?

MACRS is thought of as accelerated depreciation for two reasons: the system shortened class lives so depreciation happens more quickly, and also allows companies to deduct more of an item’s cost in the first years.

What does ACRS stand for depreciation?

The accelerated cost recovery system (ACRS) is a depreciation method for assets with the goal of providing tax breaks. ACRS was implemented in 1981 by the Internal Revenue Service (IRS) and replaced in 1986 by the modified accelerated cost recovery system (MACRS).

Is MACRS same as double declining balance?

Under MACRS, a company must use different depreciation methods for different classes of assets. For heavy machinery, MACRS requires that companies set the taxable life at 10 years and use a “double-declining” method. This method depreciates the asset by 20 percent of its value at the beginning of each tax year.

What is MACRS 200% declining balance?

200% declining balance method over a GDS recovery period – This method provides a larger deduction in the early years of an asset’s useful life and less in the later years. Refer to the MACRS Depreciation Methods table for the type of property to use this method for.

What is the 200 percent declining balance method?

The double declining balance method of depreciation, also known as the 200% declining balance method of depreciation, is a form of accelerated depreciation. This means that compared to the straight-line method, the depreciation expense will be faster in the early years of the asset’s life but slower in the later years.

Does MACRS give higher NPV?

A project that uses MACRS will have a higher NPV than the same project using straight-line depreciation. If we sell an asset at a loss, the NSV is simply the MV, as we do not have any taxes to calculate.

How does the IRS depreciate solar panels?

According to the IRS, depreciation basis is reduced by one-half of the tax credit amount allowed. For example, if you purchase solar in 2021, when the tax credit is 26%, then your depreciation basis would be 87% of the total cost of your solar (100% – [26%*.

How many years do you depreciate solar panels?

As a large purchase that will be used overtime, a solar system’s cost is deducted from taxable income via a so-called 5 year ‘depreciation’ (rather than 100% immediately as a direct ‘expense’).

What is the solar tax credit for 2021?

You can qualify for the ITC for the tax year that you installed your solar panels as long as the system generates electricity for a home in the United States. In 2021, the ITC will provide a 26% tax credit for systems installed between 2020 and 2022, and 22% for systems installed in 2023.