What does it mean when a loan balloons

By Christopher Green

A balloon loan is any financing option that includes a lump sum payment that could be scheduled at any point in the term. … Borrowers have to be prepared to pay off the remaining loan balance at the end of the loan term. Rather than being left to the end of the term, a lump-sum payment could also happen in the middle.

Is a balloon loan a good idea?

Balloon payments allow borrowers to reduce that fixed payment amount in exchange for making a larger payment at the end of the loan’s term. In general, these loans are good for borrowers who have excellent credit and a substantial income.

How do I get rid of balloon payment?

- Refinance: When the balloon payment is due, one option is to pay it off by obtaining another loan. …

- Sell the asset: Another option for dealing with a balloon payment is to sell whatever you bought with the loan.

Why do banks do balloon loans?

Since it is not fully amortized, a balloon payment is required at the end of the term to repay the remaining principal balance of the loan. Balloon loans can be attractive to short-term borrowers because they typically carry lower interest rates than loans with longer terms.What happens if you can't pay a balloon payment?

Balloon mortgages are short-term mortgage loans that usually are due and payable within five to 10 years. … If the balloon payment isn’t paid when due, the mortgage lender notifies the borrower of the default and may start foreclosure.

Are balloon mortgages legal?

A balloon payment provision in a loan is not illegal per se. Federal and state legislatures have enacted various laws designed to protect consumers from being victimized by such a loan.

Do you have to pay the balloon payment?

No, you don’t have to pay the balloon payment. At the end of a PCP car finance deal you have three options: Pay the balloon payment and become the owner of the car. Start a new finance agreement on the same car*, or get a brand new one.

How does the balloon payment work?

A balloon payment allows a buyer to take an amount owing on the purchase price of a car and set it aside, meaning the monthly instalment amounts are calculated on a lower value – in turn making repayments more affordable. You’re essentially paying off a loan for most of the car, but not all of it.Who would benefit from a balloon mortgage?

Those consumers who plan to live in a home for only a short period of time, might do well to take out a balloon mortgage. Say they plan to move in three years. They can take out a five-year balloon mortgage at a lower interest rate and then sell their home long before that massive balloon payment becomes due.

What is balloon payment?Well, a balloon payment is simply a lump sum paid at the end of a loan’s term that is larger than all of the payments made before it. Balloon payments allow those who are borrowing money to reduce the fixed payment amount in exchange for making a larger payment at the end of the loan’s term.

Article first time published onHow are balloon payments calculated?

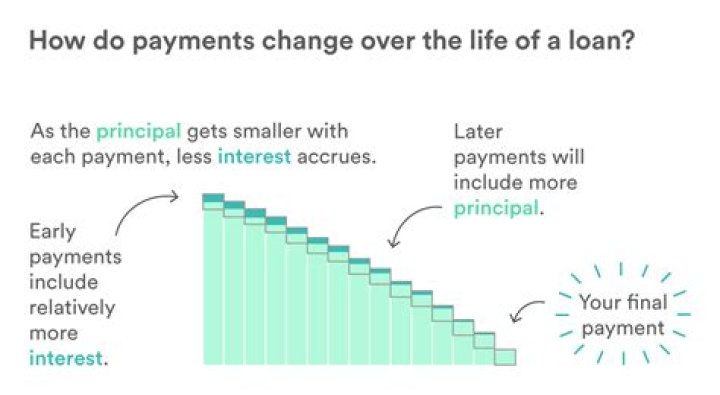

And despite its short duration, the payments are calculated based on a full amortization schedule under a 30-year mortgage. In a balloon loan, the monthly payment is not as high as regular amortizing loans with a short term. However, borrowers must prepare for the large amount to completely pay down the mortgage.

What happens when a balloon mortgage is due?

What Happens When the Balloon Payment Is Due? When your balloon payment is due, you have two choices to pay it off: You can take out another mortgage for the amount of the balloon payment or you can sell your home and use the proceeds to pay it off.

What is the minimum term for a balloon payment?

Balloon mortgages can also charge interest-only payments, which allow the borrowers to make low monthly payments before repaying the lump sum when it is due. Balloon mortgages may be issued for a term as short as two years, although terms of five to seven years are more usual.

Can I sell my home with a balloon mortgage?

A. Homeowners are permitted to sell their house with a balloon mortgage. The only caveat is that the sales price less expenses are sufficient to pay off the balloon loan.

What are the disadvantages of a balloon mortgage?

Drawbacks. Balloon mortgages carry with them a strong risk. Because they do not pay down much of the principal, mortgage holders are still faced with a significant financial obligation at the end of the loan’s life. If they cannot pay off the principal in one lump sum, they must attempt to refinance.

What is the difference between balloon payment and deposit?

In short, a balloon payment is exactly the same as paying a deposit on a motor vehicle, but with one very important difference: A deposit is paid by the vehicle buyer upfront, while a balloon payment is paid at the end of the finance period.

What is the difference between a balloon loan and an amortized loan?

A balloon loan comprises a stream of constant payments followed by a large payment at the end, which is called the balloon payment. In contrast, a fully amortized loan is composed of equal payments, which are paid through the life of the loan. The balance at the end of the payments, in such a case, is zero.

Do balloon mortgages still exist?

Balloon mortgages were far more common before the 2008-09 financial crisis. These days, most mortgages are 15- or 30-year loans with fixed interest rates. But balloon mortgages still exist.

What happens at the end of a balloon loan?

During the term of a balloon mortgage, the loan works like 15- or 30-year fixed-rate financing. … The last payment is the balloon payment. The remaining balance of the loan must be paid off in one large payment and with cash or a refinance.

Why do commercial loans have balloon payments?

Generally, loans have balloon payments to offset the lower amount of money that the borrower would put into a loan agreement. Placing a large, fixed sum final payment on the loan allows the lender to lower the interest rate and the monthly repayments while minimizing the lender’s long-term credit risk.

What makes buying a foreclosed property Risky?

One of the risks of foreclosure investing is buying a property that needs more repairs than you initially expected. In fact, foreclosed homes are typically sold «as is», meaning that the bank or the owner won’t make any repairs before putting the property up for sale.