What is a good information coefficient

By James Craig

An information coefficient (IC) score near +1.0 indicates that the analyst has great skill in forecasting.

What is an acceptable information ratio?

Generally speaking, an information ratio in the 0.40-0.60 range is considered quite good. Information ratios of 1.00 for long periods of time are rare.

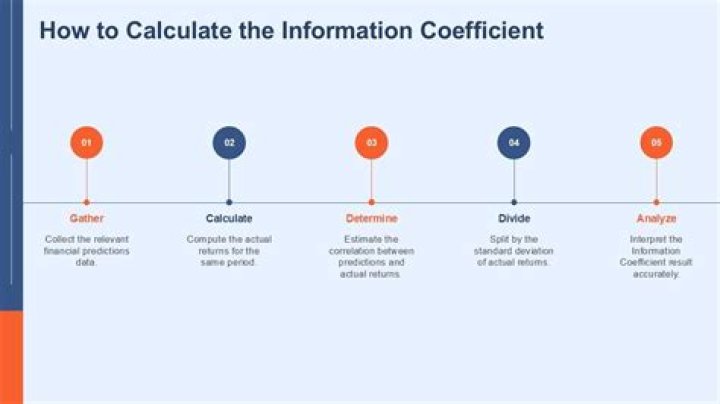

How do you find the coefficient of information?

Informational coefficient from the portfolio management section is indeed -1 to 1, calculated by IC = 2(% correct) – 1. It serves as a proxy for how correct a manager is.

What does an information ratio of 1 mean?

Information ratio measures the fund’s performance relative to its benchmark and adjusts it for market volatility. If the ratio is between 0.61 and 1, then it is a great investment.What is transfer coefficient in information ratio?

The Transfer Coefficient ∎ TC is a measure of how effectively the investor’s information is. transferred into the portfolio structure. ∎ TC is measured as the correlation between the attractiveness of the. security and its relative weight in the portfolio (adjusted for risk)

What is good Sharpe ratio?

So what is considered a good Sharpe ratio that indicates a high degree of expected return for a relatively low amount of risk? Usually, any Sharpe ratio greater than 1.0 is considered acceptable to good by investors. A ratio higher than 2.0 is rated as very good. A ratio of 3.0 or higher is considered excellent.

What is considered low tracking error?

Low tracking error means a portfolio is closely following its benchmark. High tracking errors indicates the opposite. Thus, tracking error gives investors a sense of how “tight” the portfolio in question is around its benchmark or how volatile the portfolio is relative to its benchmark.

What is a good Treynor ratio?

When using the Treynor Ratio, keep in mind: For example, a Treynor Ratio of 0.5 is better than one of 0.25, but not necessarily twice as good. The numerator is the excess return to the risk-free rate. The denominator is the Beta of the portfolio, or, in other words, a measure of its systematic risk.What is a good Jensen's Alpha?

Jensen’s measure is one of the ways to determine if a portfolio is earning the proper return for its level of risk. If the value is positive, then the portfolio is earning excess returns. In other words, a positive value for Jensen’s alpha means a fund manager has “beat the market” with their stock-picking skills.

How does an equity investor make money?Equity financing involves selling a stake in your business in return for a cash investment. Unlike a loan, equity finance doesn’t carry a repayment obligation. Instead, investors buy shares in the company in order to make money through dividends (a share of the profits) or by eventually selling their shares.

Article first time published onHow do you interpret information coefficients?

An IC of +1.0 indicates a perfect linear relationship between predicted and actual returns, while an IC of 0.0 indicates no linear relationship. An IC of -1.0 indicates that the analyst always fails at making a correct prediction.

What is CFA Level 2 transfer coefficient?

The CFA text books mentions that TC is basically the cross sectional correlation between forecasted active security returns and actual active weights adjusted for risk.

How is correlation calculated?

- Step 1: Find the mean of x, and the mean of y.

- Step 2: Subtract the mean of x from every x value (call them “a”), and subtract the mean of y from every y value (call them “b”)

- Step 3: Calculate: ab, a2 and b2 for every value.

- Step 4: Sum up ab, sum up a2 and sum up b.

What is value at risk in finance?

Value at risk (VaR) is a statistic that quantifies the extent of possible financial losses within a firm, portfolio, or position over a specific time frame. … Risk managers use VaR to measure and control the level of risk exposure.

How is Calmar ratio calculated?

Calculating the Calmar ratio To arrive at a fund’s Calmar ratio, we take its average annual rate of return over the past three years and divide it by the fund’s maximum drawdown over that same time period. So if a fund’s average annual rate of return is 50% and its maximum drawdown is 25%, its Calmar ratio is 2.

What is the ideal tracking error in a mutual fund?

If a mutual fund gives a return of 15%, while the benchmark gives 14% return, then the tracking error is 1%. Over a longer period, the standard deviation of this difference is used to measure how well the fund tracks the benchmark. Hence, tracking error also shows the consistency of the fund performance.

What does a tracking error of 1 mean?

So, for example, we could say a portfolio has a tracking error relative to its benchmark of 1% per year. For a portfolio with a normal distribution of excess returns and an annualized tracking error of 1%, we would expect its return to be within 1% of its benchmark return approximately two out of every three years.

What does a positive tracking error mean?

Tracking error is the divergence between the price behavior of a position or a portfolio and the price behavior of a benchmark. This is often in the context of a hedge fund, mutual fund, or exchange-traded fund (ETF) that did not work as effectively as intended, creating an unexpected profit or loss.

What does a Sharpe ratio of 0.5 mean?

As a rule of thumb, a Sharpe ratio above 0.5 is market-beating performance if achieved over the long run. A ratio of 1 is superb and difficult to achieve over long periods of time. A ratio of 0.2-0.3 is in line with the broader market.

Does Sharpe ratio matter?

Sharpe ratios are used extensively by hedge funds but are not typically used by individual investors. You should care about your Sharpe ratio because a low ratio means you’re almost automatically getting poor returns compared to what you could get if you allocated to better investments.

Which stock has the highest Sharpe ratio?

- Mid-America Apartment Communities, Inc. (NYSE: MAA) …

- WEC Energy Group, Inc. (NYSE: WEC) …

- Sysco Corporation (NYSE: SYY) Number of Hedge Fund Holders: 40 Dividend Yield: 2.4% Sharpe Ratio: 1.2. …

- Broadcom Inc. (NASDAQ: AVGO) …

- Xcel Energy Inc. (NASDAQ: XEL)

What is a good Jensen's measure?

ManagerAverage Annual ReturnBetaManager F15%1.20

What is a good Jensen's alpha number?

For investors wishing to use benchmarks to measure returns, Jensen’s alpha is the choice for them. If Walmart shows a 2% alpha, that indicates that Walmart is beating its benchmark by 2%. So the higher the alpha, the better.

Does higher beta mean more risk?

What Is Beta? Beta is a measure of a stock’s volatility in relation to the overall market. … High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

Is a higher Treynor ratio better?

In essence, the Treynor ratio is a risk-adjusted measurement of return based on systematic risk. … A higher ratio result is more desirable and means that a given portfolio is likely a more suitable investment.

What is a good Alpha?

Defining Alpha Alpha is also a measure of risk. An alpha of -15 means the investment was far too risky given the return. An alpha of zero suggests that an asset has earned a return commensurate with the risk. Alpha of greater than zero means an investment outperformed, after adjusting for volatility.

What is the Treynor ratio of the S&P 500?

InvestmentReturnBetaS&P 500 Index10%1.00Fancy Fund12%0.9Risks for Reward Fund22%2.5

How can I invest 100 dollars to make money?

- Start an emergency fund.

- Use a micro-investing app or robo-advisor.

- Invest in a stock index mutual fund or exchange-traded fund.

- Use fractional shares to buy stocks.

- Put it in your 401(k).

- Open an IRA.

What is the best investment for beginners?

- High-yield savings accounts. This can be one of the simplest ways to boost the return on your money above what you’re earning in a typical checking account. …

- Certificates of deposit (CDs) …

- 401(k) or another workplace retirement plan. …

- Mutual funds. …

- ETFs. …

- Individual stocks.

Do equity investors get paid monthly?

No Interest Payments – You do not need to pay your investors interest, although you will owe them some portion of your profits down the road. … No Monthly Payments – You probably won’t need to make monthly payments until you make a profit – which keeps more cash in your pocket while you get things up and running.

What is active risk in a portfolio?

Active risk is a type of risk that a fund or managed portfolio creates as it attempts to beat the returns of the benchmark against which it is compared. Risk characteristics of a fund versus its benchmark provide insight on a fund’s active risk.