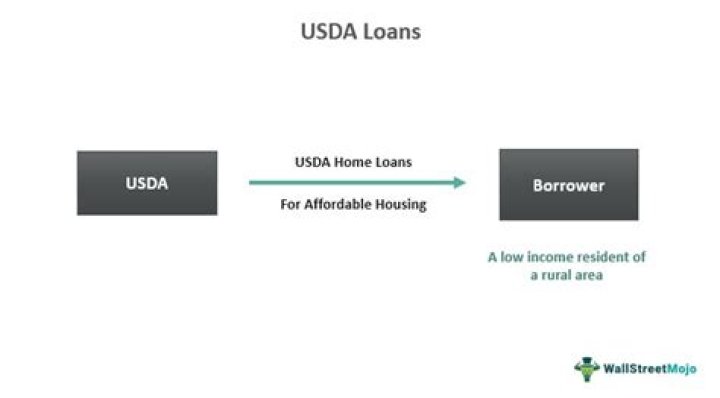

What is a USDA loan and who qualifies

By Olivia Bennett

USDA loans are low-interest mortgages with zero down payments designed for low-income Americans who don’t have good enough credit to qualify for traditional mortgages. You must use a USDA loan to buy a home in a designated area that covers several rural and suburban locations.

What is the minimum income for a USDA loan?

USDA eligibility for a 1–4 member household requires annual household income to not exceed $91,900 in most areas of the country, and annual household income for a 5–8 member household to not exceed $121,300 for most areas. This USDA loan information is accurate as of today, January 1, 2022.

How do you know if a home qualifies for a USDA loan?

Verify a Home’s Address for a USDA Loan If your prospective home falls near or in an area that does not appear to meet the rural designation, a USDA-approved lender can verify the address through the USDA’s online portal. To verify your address for a USDA loan, it is best to speak with a USDA-approved lender.

What is bad about USDA loans?

Disadvantages of USDA Loans These include: Geographical requirements: Homes must be located in an eligible rural area with a population of 35,000 or less. Also, the home cannot be designed for income-producing activities, which could rule out certain rural properties.What's the difference between a USDA loan and a regular loan?

Conventional loans are available nationwide. USDA loans, on the other hand, are only available in eligible rural areas as determined by the USDA. If you’re located in a major metropolitan area, you likely won’t be able to get a USDA loan.

What is the max loan amount for USDA?

As of May 12, 2021, the standard USDA loan income limit for 1-4 member households is $91,900 or $121,300 for 5-8 member households in most U.S. counties. Total household income should not exceed these limits to be eligible for a USDA home loan, but income limits can vary by location to account for cost of living.

What is Max income for USDA loan?

USDA Loan Income Limits and Eligibility in 2021 To be eligible for a USDA home loan, your total household income cannot exceed the local USDA income limits. The current standard USDA loan income limit for 1-4 member households is $91,900, up from $90,300 in 2020.

What is the annual fee for USDA loans?

The USDA Loan fees for FY 2021 are: an upfront guarantee fee of 1.0% of the loan amount, and an annual fee of 0.35% of the loan amount. These fees apply to both home purchases and refinance transactions during the 2021 fiscal year, which runs October 1, 2020 through September 30, 2021.Do sellers like USDA loans?

Sellers should have no concerns about accepting a USDA buyer’s offer. Like many things in regards to mortgages, a lot comes down to the lender and their ability to communicate and close loans efficiently.

What are my chances of getting a USDA loan?To get a USDA loan, you have to meet certain requirements: Your income must be within 115% of the median household income limits specified for your area (find out if you’re eligible here) You must be a U.S. citizen or permanent resident (green card holder) You will likely need a credit score 640 or above.

Article first time published onHow long does it take for a USDA loan to be approved?

Once you’ve signed a purchase agreement, the USDA loan application process typically takes around 30-45 days. The faster all parties work together to complete and provide documents for loan approval, the quicker final loan approval and closing can happen.

What credit score do you need for USDA loan?

The USDA doesn’t have a fixed credit score requirement, but most lenders offering USDA-guaranteed mortgages require a score of at least 640, and 640 is the minimum credit score you’ll need to qualify for automatic approval through the USDA’s automated loan underwriting system.

Are FHA and USDA loans the same?

USDA and FHA loans are run by two different government agencies, which means they have different application, underwriting, appraisal, lending amount, mortgage insurance and interest rate requirements.

Is it easy to get approved for a USDA loan?

The USDA home loan is available to borrowers who meet income and credit eligibility requirements. Qualification is easier than for many other loan types, since the loan doesn’t require a down payment or a high credit score.

Does USDA have a maximum sales price?

Since there is no maximum sales price for a USDA loan, this means there is also NO maximum mortgage loan limit! Instead, the USDA maximum loan amount is calculated based on the applicant’s ability to qualify. Thankfully, USDA income limits have increased as of May 4th, 2020.

Who pays closing costs on USDA loan?

USDA Closing Costs Paid By Seller Rather than bringing more cash to close, USDA loans allow the seller to pay up to 6% of the sales price towards the buyer’s closing costs. Therefore, the seller may pay part or all of the buyer’s closing costs.

Who pays for the appraisal on a USDA loan?

Who pays for a USDA inspection (and how much does it cost)? It will vary by lender, but the USDA does allow lenders to pass the cost of the appraisal to the buyer. It may also be included in your closing costs. Typically, a USDA appraisal costs between $400 and $500.

Are USDA loans hard to close?

With an FHA, VA, or conventional loan, the lender can completely approve and close the loan on its own. USDA, however, requires a hands–on check by USDA staff. The process can take an extra few days or up to three weeks or more depending on the backlog at your state’s USDA office.

Is USDA funded for 2021?

2021 FUNDING OVERVIEW Funding for mandatory programs is estimated to be $128 billion, $3 billion more than 2020 enacted levels. Including negative receipts, offsetting collections, recoveries, etc., USDA is requesting a total of $146 billion in 2021 available funds.

What is the monthly USDA fee?

In 2019 the fee is set at 0.35% of the annual unpaid loan balance. This fee is typically charged to the lender by the USDA and it’s then passed along to the borrower to be paid monthly out of an escrow account.

Is there monthly PMI on USDA loans?

No, USDA loans do not require private mortgage insurance, or PMI, as PMI only applies to conventional loans. … The upfront fee is paid at closing and is rolled into the loan amount, while the annual fee is calculated once per year and then divided into monthly payments along with other monthly costs.

How do I start a USDA loan?

- Prequalify with a USDA-approved lender.

- Apply for preapproval.

- Find a USDA-approved home.

- Sign a purchase agreement.

- Go through processing and underwriting.

- Close on your loan.

Do you have to pay back a USDA loan?

The USDA mortgage does NOT have any prepayment or early payoff penalty. You can sell/pay off your loan whenever you like without restriction or fees. This is also the case with other Government-backed loans like FHA and VA.

Is homeowners insurance included in USDA loan?

Paying Homeowners and Flood Insurance Premiums For a USDA loan, you have to have homeowners insurance coverage for the amount of the loan or what it would cost to completely replace your house if it was destroyed. … At closing, you will pay the entire first year’s premiums as part of your closing costs.

Is FHA or USDA cheaper?

With no down payment requirement and low mortgage insurance rates, USDA mortgages are often cheaper both upfront and in the long run than FHA loans. USDA may be cheaper than conventional financing, too, if you have a credit score in the low 600’s and a small down payment.

Is it easier to get a USDA loan or FHA?

FHA loans can be better if you have a lower credit score, but USDA loans don’t require a down payment. Mortgage loans from the United States Department of Agriculture (USDA) and Federal Housing Administration (FHA) are generally easier to qualify for than a conventional mortgage.