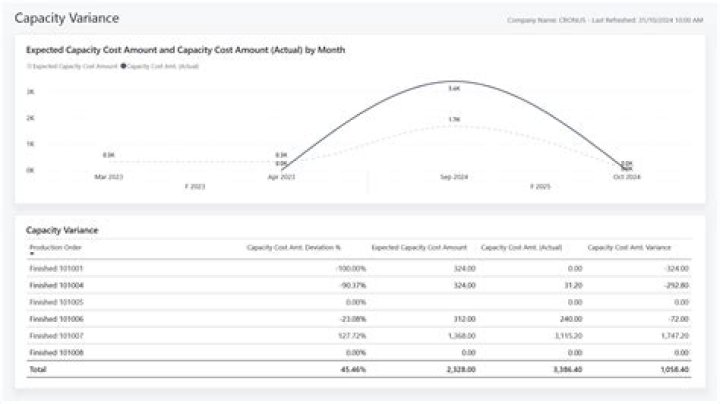

What is meant by capacity variance

By Christopher Green

The idle capacity variance is the amount by which actual production usage declines below the normal or expected production level, multiplied by the overhead application rate. For example, a machine has a normal, long-term usage level of 400 hours per month (essentially two shifts of work per business day).

What does fixed overhead capacity variance mean?

Fixed overhead volume variance is the difference between the amount budgeted for fixed overhead costs based on production volume and the amount that is eventually absorbed. This variance is reviewed as part of the cost accounting reporting package at the end of a given period.

What is controllable variance?

A controllable variance refers to the “rate” portion of a variance. … Or, stated another way, the controllable variance is actual expenses minus the budgeted amount of expenses for the standard number of units allowed.

What is overhead capacity?

In a system of standard costing, the difference arising between the actual hours worked and the budgeted capacity available, valued at the standard fixed overhead absorption rate per hour. It can be measured in machine hours or labour hours. See capacity; idle capacity; idle capacity ratio.How do you calculate production volume variance?

The formula for production volume variance is as follows: Production volume variance = (actual units produced – budgeted production units) x budgeted overhead rate per unit.

What is sales margin variance?

This is the difference between the standard margin appropriate to the quantity of sales budgeted for a period, and the margin between standard cost and the actual selling price of the sales effected.

What is budget variance?

A variance is the difference between actual and budgeted income and expenditure.

What is flexible budget variance?

A flexible budget variance is any difference between the results generated by a flexible budget model and actual results. If actual revenues are inserted into a flexible budget model, this means that any variance will arise between budgeted and actual expenses, not revenues.How is expenditure variance calculated?

- Actual cost – expected cost = spending variance.

- (Actual variable overhead rate – expected variable overhead rate) x hours worked = variable overhead spending variance.

A cost variance is the difference between an actual and budgeted expenditure. … The cost variance formula is usually comprised of two elements, which are: Volume variance. This is the difference in the actual versus expected unit volume of whatever is being measured, multiplied by the standard price per unit.

Article first time published onWhy is volume variance uncontrollable?

The production volume variance is said to be uncontrollable because control refers to influence over actual costs. The production volume variance is the difference between budgeted and applied fixed overhead. … The price variance based on quantity purchased and the price variance based on quantity used in production.

What is total overhead variance?

Overhead cost variance can be defined as the difference between the standard cost of overhead allowed for the actual output achieved and the actual overhead cost incurred. In other words, overhead cost variance is under or over absorption of overheads.

Which of the following is the another name of material usage variance?

The materials usage variance, which is also referred to as the materials quantity variance, is associated with a standard costing system.

What is product variance?

Also known as loss or shrinkage, variance reflects the difference between the number of products sold over a period of time and the number of product used over that same period. Simply put, it allows you to identify which inventory items were lost or overpoured.

What is mix variance?

Sales mix variance is the difference between a company’s budgeted sales mix and the actual sales mix. … Sales mix affects total company profits because some products generate higher profit margins than others. Sales mix variance includes each product line sold by the firm.

What is manufacturing volume variance?

The production volume variance measures the amount of overhead applied to the number of units produced. It is the difference between the actual number of units produced in a period and the budgeted number of units that should have been produced, multiplied by the budgeted overhead rate.

What variance means?

Definition of variance 1 : the fact, quality, or state of being variable or variant : difference, variation yearly variance in crops. 2 : the fact or state of being in disagreement : dissension, dispute. 3 : a disagreement between two parts of the same legal proceeding that must be consonant.

What does YTD variance mean?

Budget variance analysis can create a more accurate forecast for year to date (YTD) and end of year (EOY). Your summary YTD shows how you have performed. It also shows how you will perform compared to budget for the remainder of the year.

What are the types of variances?

- Sales variance.

- Direct material variance.

- Direct labour variance.

- Overhead variance.

How do you calculate price and volume variance?

- (2018 Selling price – 2017 Selling price) x Units sold in 2018.

- Apples sold at 2018 Price – Apples sold at 2017 Price.

- Sales Volume Variance =

- (2018 Units Sold – 2017 Units Sold) x 2017 Profit Margin per Unit.

What is sales margin?

Sales margin is the amount of profit generated from the sale of a product or service. It is used to analyze profits at the level of an individual sale transaction, rather than for an entire business.

What is sales price variance?

Sales price variance refers to the difference between a business’s expected price of a product or service and its actual sales price.

How does maximum capacity differ from normal capacity?

4.2 ‘Installed Capacity’ is the maximum productive capacity according to the manufacturers’ specification of machines / equipment. … Normal capacity is practical capacity minus the loss of productive capacity due to external factors.

What is the difference between flexible budget variance and sales volume variance?

This is a flexible budget based on the actual sales level. Then the price cost variances are the differences between the actual results and the flexible budget, i.e., columns 2 and 4. The sales volume variances are the differences between the static master budget and the flexible budget, i.e., columns 1 and 4.

What is flexed budget with example?

This type of budget is most often based on changes in a company’s actual revenue and uses percentages of revenue rather than static numbers. For example, a flexible budget may allot 25% of a company’s revenue to salary as opposed to allotting $100,000 to salary in a given year.

What is static budget variance?

1. Static Budget Variance: The difference between the actual results and the static budget. 2. Sales Volume Variance: The difference between the flexible budget and the static budget. These variances are used to assess whether the differences were favorable (increased profits) or unfavorable (decreased profits).

What is volume variance and spending variance?

The fixed overhead spending variance is the difference between actual and budgeted fixed overhead costs. The fixed overhead production volume variance is the difference between budgeted and applied fixed overhead costs.

How is the idle capacity variance calculated?

Capacity can be measured in machine hours or labour hours and idle capacity is measured in the same way. The formula is:(budgeted hours – actual hours worked × 100)/budgeted hours.

What causes favorable material usage variance?

Reasons for a favorable material usage variance may include: Purchase of materials of higher quality than the standard (this will be reflected in adverse material price variance). Greater use of skilled labor. Training and development of workforce to improve productivity.

Why material usage variance occurs?

A usage variance can arise from any of the following issues: An incorrect standard against which actual usage is measured. Not changing the bill of materials after a production process or product design has been altered that should have resulted in a change in the amount of materials usage.

What is the formula of material yield variance?

The Formula to calculate Material Quantity Variance = (Actual quantity used × Standard rate) – (Standard quantity allowed/estimated × Standard rate).