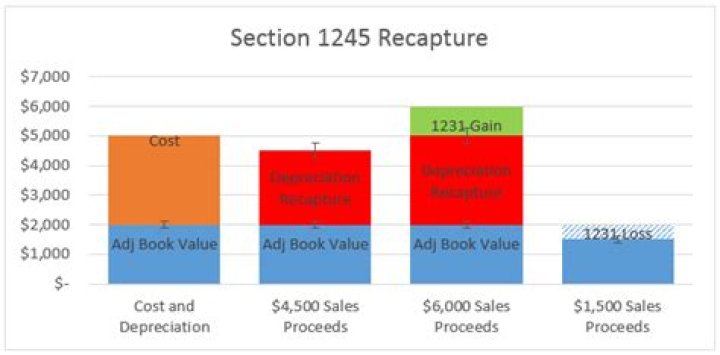

What is Section 1245 depreciation recapture

By Andrew Hansen

Section 1245 recaptures depreciation or amortization allowed or allowable on tangible and intangible personal property at the time a business sells such property at a gain. Section 1245 taxes the gain at ordinary income rates to the extent of its allowable or allowed depreciation or amortization.

How is Section 1245 recapture taxed?

When a business or real estate investment is sold, 1245 property that was depreciated must be recaptured. The recaptured depreciation is taxed as ordinary income up to one of the following: The allowed or allowable depreciation or amortization on the property. The gain realized on the sale or disposition.

How do you avoid depreciation recapture on rental property?

Investors may avoid paying tax on depreciation recapture by turning a rental property into a primary residence or conducting a 1031 tax deferred exchange. When an investor passes away and rental property is inherited, the property basis is stepped-up and the heirs pay no tax on depreciation recapture or capital gains.

How is 1245 depreciation recapture calculated?

Section 1245 recapture is computed as the lesser of: (1) allowable depreciation or amortization on the disposed assets, or (2) the gain realized upon the disposition.Can you avoid depreciation recapture?

There are ways in which you can minimize or even avoid depreciation recapture. One of the best ways is to use a 1031 exchange, which references Section 1031 of the IRS tax code. This may help you avoid depreciation recapture and any capital gains taxes that might apply.

How does depreciation recapture work?

Depreciation recapture is a tax provision that allows the IRS to collect taxes on any profitable sale of an asset that the taxpayer had used to previously offset taxable income. … To calculate the amount of depreciation recapture, the adjusted cost basis of the asset must be compared to the sale price of the asset.

When a result results the sale of section 1245 property?

When a gain results from the sale of Section 1245 property, how does the taxpayer determine the amount that should be taxed as ordinary income? The lesser of the recognized gain or the accumulated depreciation on the asset is ordinary income. The current year’s depreciation is recaptured as ordinary income.

What is the theory behind Sections 1245 and 1250?

Sections 1245 and 1250 were enacted to close the loophole that resulted from allowing depreciation deductions on assets to offset ordinary income while taxing gain from the sale of these depreciated assets as capital gains.What is the difference between Section 1245 and 1250 property?

Section 1245 assets are depreciable personal property or amortizable Section 197 intangibles. Section 1250 assets are real property, where depreciable or not.

How do you calculate depreciation recapture?You could then determine the asset’s depreciation recapture value by subtracting the adjusted cost basis from the asset’s sale price. If you bought equipment for $30,000 and the IRS assigned you a 15% deduction rate with a deduction period of four years, your cost basis is $30,000.

Article first time published onWhat happens when rental property is fully depreciated?

It depends but in this instance, the residential rental property will be considered fully depreciated after 27.5 year. … According to the IRS, You must stop depreciating property when the total of your yearly depreciation deductions equals your cost or other basis of your property.

How long do I have to live in my rental property to avoid capital gains?

If you like your rental property enough to live in it, you could convert it to a primary residence to avoid capital gains tax. There are some rules, however, that the IRS enforces. You have to own the home for at least five years. And you have to live in it for at least two out of five years before you sell it.

Does 1031 avoid depreciation recapture?

1031 Exchanges allow you to defer both the capital gains tax and depreciation recapture from the sale of a property and invest the proceeds into another “like-kind” property, often called “trading up.”

When you sell an investment property do you have to pay back depreciation?

The depreciation deduction lowers your tax liability for each tax year you own the investment property. It’s a tax write off. But when you sell the property, you’ll owe depreciation recapture tax. You’ll owe the lesser of your current tax bracket or 25% plus state income tax on any deprecation you claimed.

What can offset depreciation recapture?

Depreciation recapture on real property is nothing more than a specially taxed type of capital gain. As such, it can be offset by capital losses. Real property used in a trade or business or held out for rental is subject to an allowance for depreciation.

Do I take depreciation in the year of sale?

First, to establish account balances that are appropriate at the date of sale, depreciation is recorded for the period of use during the current year. … Second, the amount received from the sale is recorded while the book value of the asset (both its cost and accumulated depreciation) is removed.

What is a 1245 property?

Generally, 1245 property is known as “tangible” or “personal” property. 1245 tangible property assets are depreciated over shorter depreciable lives mandated by the Internal Revenue Service (IRS). … Personal property does not include a building or any of the structural components of a building.

When an installment sale involves Section 1245 depreciation recapture how is the gain recognized?

When an installment sale involves Sec 1245 depreciation recapture, how is the gain recognized? The portion of gain due to recapture is recognized immediately. Any remaining Sec. 1231 gain can be recognized on the installment method.

When an installment sale involves Section 1245 depreciation recapture how is the gain recognized multiple choice question?

The gain arising due to depreciation recapture is recognized in the income tax returns immediately. Section 1231 is used to report the capital gains arising from property sales using the installment method. This section applies to those properties that are depreciable and held for more than one year.

What happens when you sell a depreciated asset?

Selling Depreciated Assets When you sell a depreciated asset, any profit relative to the item’s depreciated price is a capital gain. For example, if you buy a computer workstation for $2,000, depreciate it down to $800 and sell it for $1,200, you will have a $400 gain that is subject to tax.

Why does 1250 recapture generally no longer apply?

Why does §1250 recapture generally no longer apply? … §1245 recapture trumps §1250 recapture. Because unrecaptured §1250 gains now apply to all taxpayers instead. The Tax Reform Act of 1986 changed the depreciation of real property to the straight-line method.

Do you recapture depreciation on 1250 property?

Gain from selling Sec 1250 property (real estate) is subject to recapture – the excess of the actual amount of depreciation previously claimed for the property over the amount of depreciation that would have been allowable under the straight-line method, limited to the gain on the sale, is taxed as ordinary income.

Is rental property 1245?

Any depreciable property that is not section 1245 property is by default section 1250 property. … The most common examples of section 1250 property are commercial buildings (MACRS 39-year real property) and residential rental property (MACRS 27.5-year residential rental property).

What is section 1250 gain recapture?

An unrecaptured section 1250 gain is an income tax provision designed to recapture the portion of a gain related to previously used depreciation allowances. It is only applicable to the sale of depreciable real estate. Unrecaptured section 1250 gains are usually taxed at a 25% maximum rate.

Does depreciation recapture apply to personal property?

Because personal property depreciates on a faster scale than real property, avoidance of depreciation recapture is often the reason for structuring a Personal Property Exchange, and many do not realize that taxable gains on these properties can be deferred.

What are 1250 Assets?

Section 1250 addresses the taxing of gains from the sale of depreciable real property, such as commercial buildings, warehouses, barns, rental properties, and their structural components at an ordinary tax rate. However, tangible and intangible personal properties and land acreage do not fall under this tax regulation.

How do I report depreciation recapture on my tax return?

The recapture amount is included on line 31 (and line 13) of Form 4797. See the instructions for Part III. If the total gain for the depreciable property is more than the recapture amount, the excess is reported on Form 8949.

What does recapture mean in real estate?

Recapture allows a seller of some asset or property to reclaim some or all of it at a later date. The seller will have the option to buy back what has been sold, within a certain window of time, often at a higher price than what it was initially sold for.

What happens if you never took depreciation on a property and then sold it?

You should have claimed depreciation on your rental property since putting it on the rental market. If you did not, when you sell your rental home, the IRS requires that you recapture all allowable depreciation to be taxed (i.e. including the depreciation you did not deduct).

What is the 6 year rule?

The six-year rule allows you to move out of your residence, rent somewhere else and rent out your former home, and then sell it before the six-year period is up without having to pay CGT.

What is the capital gain tax for 2020?

Capital Gains Tax RateTaxable Income (Single)Taxable Income (Married Filing Separate)0%Up to $40,000Up to $40,00015%$40,001 to $441,450$40,001 to $248,30020%Over $441,450Over $248,300