What is tolerable misstatement in auditing

By Emily Sparks

A tolerable misstatement is the amount by which a financial statement line item can differ from its true amount without impacting the fair presentation of the entire financial statements. The concept is used by auditors when designing audit procedures to examine the financial statements of a client.

What is the difference between tolerable misstatement and performance materiality?

In other words, tolerable misstatement is an example of performance materiality that auditors apply in the selection and evaluation of the result of the sampling. … In this case, the tolerable misstatement is always lower or equal to the actual performance materiality in the population of accounts or balances.

What are the types of misstatements in auditing?

Three types of misstatement include factual misstatement, judgmental misstatements, and projected misstatements.

How do you calculate tolerable misstatement?

9. In determining tolerable misstatement and planning and performing audit procedures, the auditor should take into account the nature, cause (if known), and amount of misstatements that were accumulated in audits of the financial statements of prior periods.What is planning materiality and tolerable error?

Tolerable error is the maximum error the auditor is willing to accept in a population. Tolerable error is an idea that allows the auditor to put on planning materiality at the level of the individual account balance. The idea is used to: Determine the significance of accounts.

How do you calculate misstatement?

The ratio method. In this method, the value of the misstatement found in the sample (excluding high value and key items) is multiplied by the population value and divided by the value of the sample to obtain the projected misstatement in a population.

What is the risk of material misstatement in financial statement?

Risk of material misstatement is defined as ‘the risk that the financial statements are materially misstated prior to audit.

What is PM in auditing?

Performance Materiality PM means the amount or amounts set by the. auditor at LESS THAN materiality OM for the financial statements as a.What is ISI in auditing?

auditor’s professional judgment. Tolerable misstatement is abbreviated as TM; the lower. limit for individually significant items is abbreviated as LL of ISIs.

What is rule of thumb in audit?Auditors make decisions based upon a 5% rule. Misstatements of less than 5% have no effect on financial statement fairness. The 5% rule is widely used in practice.

Article first time published onWhat is a misstatement in audit?

(a) Misstatement – A difference between the amount, classification, presentation, or disclosure of a reported financial statement item and the. amount, classification, presentation, or disclosure that is required for the. item to be in accordance with the applicable financial reporting framework.

What does misstatement mean in auditing?

A misstatement is the difference between the required amount, classification, presentation, or disclosure of a financial statement line item and what is actually reported in order to achieve a fair presentation, as per the applicable accounting framework.

What are the two types of misstatements?

Two types of misstatements are relevant to the auditor’s consideration of fraud in a financial statement audit—misstatements arising from fraudulent financial reporting and misstatements arising from misappropriation of assets.

What is known misstatement?

What is a known misstatements? Definition. a misstatement where the auditor can determine the amount of the misstatement in the account. Term.

What is projected misstatement?

Projected misstatements are the auditor’s best estimate of misstatements in populations, involving the projection of misstatements identified in audit samples to the entire populations from which the samples were drawn.

What is a material misstatement?

A material misstatement is information in the financial statements that is sufficiently incorrect that it may impact the economic decisions of someone relying on those statements.

What are the 3 types of audit risk?

There are three common types of audit risks, which are detection risks, control risks and inherent risks. This means that the auditor fails to detect the misstatements and errors in the company’s financial statement, and as a result, they issue a wrong opinion on those statements.

How do auditors identify and assess risk of material misstatement?

The objective of the auditor is to identify and assess the risks of material misstatement, whether due to fraud or error, at the financial statement and assertion levels, through understanding the entity and its environment, including the entity’s internal control, thereby providing a basis for designing and …

At what two levels does the auditor assess the risk of material misstatement?

The risk of material misstatement refers to the risk that the financial statements are materially misstated and do not present true and fair view. The risk of material misstatement is assessed at two levels (i) financial statements level and (ii) assertions level.

What is sad in audit?

One of the more potentially divisive items included in the Auditor’s Report to the Audit Committee is the Summary of Audit Differences (SADs). … SADs are a mechanism used by the auditor to quantify differences in an audit. They are not meant to be a commentary on the qualitative aspects of management.

What does a higher performance materiality mean?

Thus, performance materiality reduces the probability that the aggregate amount of uncorrected and undetected misstatements exceeds the materiality level for the financial statements as a whole. … The level of performance materiality can be set at different levels for different accounts.

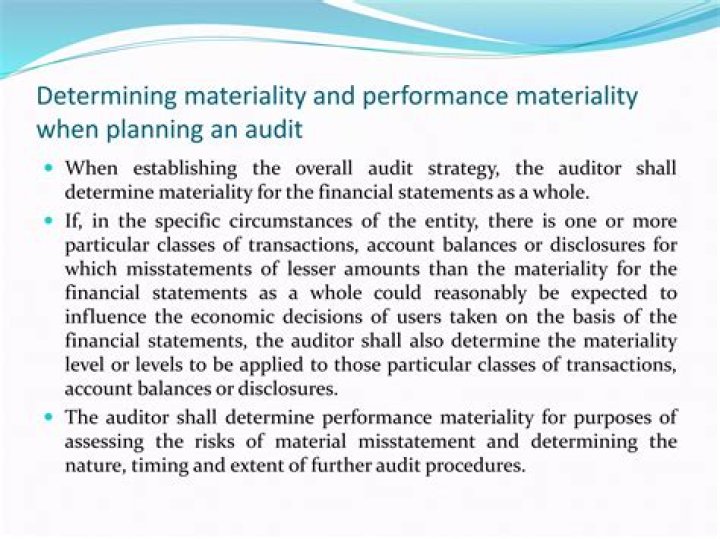

What is PSA 320?

PSA 320 (Revised and Redrafted) Introduction. Scope of this PSA. 1. This Philippine Standard on Auditing (PSA) deals with the auditor’s responsibility to apply the concept of materiality in planning and performing an audit of financial statements.

What is an ISO audit?

An ISO quality audit is a management tool companies use to evaluate, confirm, and verify activities related to quality. The ISO 9000 quality audit determines the effectiveness of an organization’s quality management system (QMS). … The ISO 9001 quality audit is the most common ISO standard for audits.

How do you select Materialmark for benchmarking?

- Total revenues.

- Total assets.

- Gross profit.

- Net profit before tax.

- Total expenses.

What is threshold in auditing?

The materiality threshold in audits refers to the benchmark used to obtain reasonable assurance that an audit does not detect any material misstatement that can significantly impact the usability of financial statements.

What is immaterial accounting?

Immaterial in accounting is a concept that addresses information that is neither relevant nor useful.

What is full disclosure principle?

As one of the principles in GAAP, the full disclosure principle definition requires that all situations, circumstances, and events that are relevant to financial statement users have to be disclosed. In other words, all of a company’s financial records and transactions have to be available for viewing.

What is material ATI principle?

The materiality principle states that an accounting standard can be ignored if the net impact of doing so has such a small impact on the financial statements that a user of the statements would not be misled.

What are some good rules of thumb?

- IF IT TAKES TWO MINUTES OR LESS, DO IT NOW. …

- KEEP YOUR IMPORTANT DOCUMENTS SAFE AND ORGANIZED. …

- RESTOCK HOUSEHOLD SUPPLIES BEFORE THEY RUN OUT. …

- GET ENOUGH SLEEP. …

- LOOK TOWARDS THE FUTURE. …

- PAY YOURSELF FIRST. …

- QUIT MULTITASKING. …

- LIVE A BALANCED LIFE.

What is rule of thumb method?

The definition of a rule of thumb is a generally accepted guideline, policy or method of doing something based on practice rather than facts. … A general guideline, rather than a strict rule; an approximate measure or means of reckoning based on experience or common knowledge.

What are the types of audit opinions?

- Unqualified opinion-clean report.

- Qualified opinion-qualified report.

- Disclaimer of opinion-disclaimer report.

- Adverse opinion-adverse audit report.