What percentage of coverage A is Coverage C

By Andrew Hansen

The limit on Coverage C protection is typically 50 percent of the Coverage A amount. Additionally, all standard homeowners policies include various “additional coverages” for items such as debris removal, trees, and shrubs.

How is coverage c calculated?

Usually, your Coverage C limit is 50% and 70% percent of your dwelling’s value. If you have $300,000 in coverage for your home, you will often get $150,000 – $210,000 in coverage on your personal belongings.

What is coverage AB and C?

Coverage B: Other Structures. Covers damage to other structures or buildings, such as a detached garage, work shed, or fencing. Coverage C: Personal Property.

What percent of Coverage A is coverage D?

Coverage D — Loss of Use Coverage D is normally limited to 20 percent of Coverage A.What is Coverage C on a condo policy?

Personal property coverage, which is Coverage C within home insurance policies, helps to pay for your personal items that have been damaged, destroyed or stolen due to a covered peril. It’s standard protection within many home insurance policies and is pivotal to cover those personal items that mean the most to you.

What are the 3 basic levels of coverage that exist for homeowners insurance?

Homeowners insurance policies generally cover destruction and damage to a residence’s interior and exterior, the loss or theft of possessions, and personal liability for harm to others. Three basic levels of coverage exist: actual cash value, replacement cost, and extended replacement cost/value.

What property is not covered under Coverage C?

Coverage C exclusions Coverage C protects all the insured’s personal property, except for the following: Motor vehicles and their equipment. Cars have their own insurance policies, so home insurance excludes them.

What does DP 2 cover?

A DP2 policy covers damage to the primary structure as well as other structures on the property, such as sheds, fences, detached garages, and patio coverings.Which is true of coverage C of the dwelling policy?

Which is true regarding Dwelling policies? Coverage C applies while insured property is located at the described location – Coverage C may be extended to cover property of guests and servants. Coverage D, Fair Rental Value, is an indirect coverage.

What area is not protected by most homeowners insurance?Termites and insect damage, bird or rodent damage, rust, rot, mold, and general wear and tear are not covered. Damage caused by smog or smoke from industrial or agricultural operations is also not covered. If something is poorly made or has a hidden defect, this is generally excluded and won’t be covered.

Article first time published onWhat is covered under Coverage B?

Coverage B, also known as other structures insurance coverage, is the part of your homeowners policy that protects structures on your property not physically connected to your home, such as a detached garage, storage shed, or gazebo.

What are the six categories covered by homeowners insurance?

- Property Damage. This covers damage to your home , such as from fire, wind, or hail. …

- Additional Living Expenses. …

- Personal Liability. …

- Medical Payment Coverage.

What is the standard liability limit for coverage E?

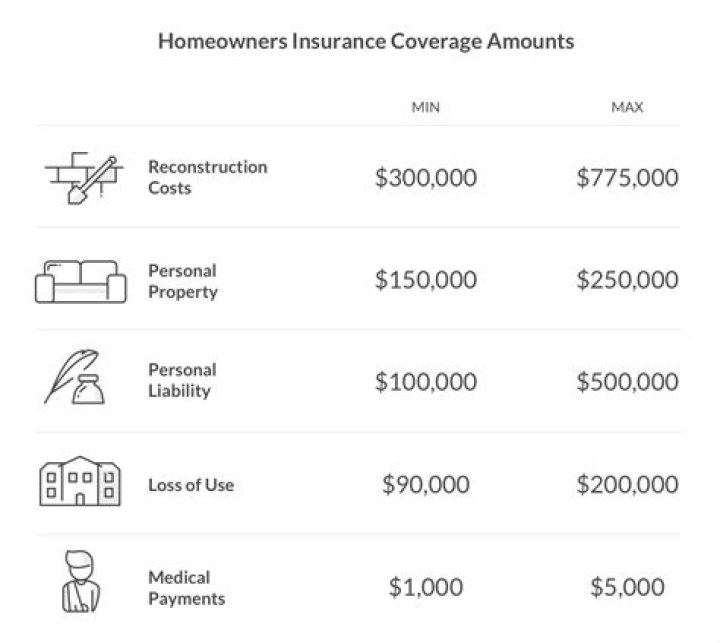

Coverage E Personal Liability Limit On Home Insurance The minimum limit of Coverage E on home insurance policies is typically $100,000 and the maximum most companies will cap you at is $500,000. However, you can get $1 million or more in personal liability coverage if you invest in umbrella insurance.

How much coverage C do I need?

You need as much personal property coverage to replace all of your personal belongings, to an extent that you can comfortably live with and afford, in case everything was destroyed by a covered peril. So if you own $30,000 worth of belongings, you’d need $30,000 worth of Coverage C personal property.

What is Walls in coverage for condos?

Walls In: Also referred to as “single entity coverage” or “studs in” refers to real property coverage from the exterior framing inward, including fixtures. However, this would not include alterations, appliances or other property types contained within the walls of a condo unit.

How much loss of use coverage do I need?

How much loss of use coverage do I need? Your loss of use coverage limit is typically about 20% to 30% of your home’s insured value, or your dwelling amount. That means if your home is insured for $400,000, your additional living expenses coverage will typically be anywhere from $80,000 to $120,000.

What is not usually covered by homeowners insurance?

What Standard Homeowner Insurance Policies Don’t Cover. Standard homeowners insurance policies typically do not include coverage for valuable jewelry, artwork, other collectibles, identity theft protection, or damage caused by an earthquake or a flood.

How much should my house be insured for?

Most homeowners insurance policies provide a minimum of $100,000 worth of liability insurance, but higher amounts are available and, increasingly, it is recommended that homeowners consider purchasing at least $300,000 to $500,000 worth of liability coverage.

What is the most important part of homeowners insurance?

The most important part of homeowners insurance is the level of coverage. Avoid paying for more than you need. Here are the most common levels of coverage: HO-2 – Broad policy that protects against 16 perils that are named in the policy.

How much will the dwelling policy pay for living expenses after a dwelling insured for $100000?

Many insurance companies set reimbursement limits that are tied to the dwelling’s property coverage total; around 20 to 50%. A dwelling that’s insured for $100,000, with a loss of use limit of 30%, will receive up to $30,000 to cover temporary living expenses.

What are the four most common endorsements for dwelling policies?

- Earthquake endorsement. Most home insurance policies exclude damage caused by earthquakes. …

- Sewer backup endorsement. …

- Scheduled personal property endorsement. …

- Home-based business endorsement. …

- Watercraft endorsement.

Which is true of coverage C of the dwelling policy quizlet?

Which is true regarding dwelling policies? Coverage C extends to property of guests and servants. Property of tenants and boarders is not covered. The Basic Dwelling Form (DP-1) provides coverage for Fair Rental Value.

What is a DP 1 policy?

A DP1 policy is a type of home insurance that protects rental or vacant homes from nine named perils. It covers the property for its actual cash value, not replacement cost.

What is the difference between DP1 DP2 and DP3 insurance?

DP2 Policy is Average Protection The DP1 is the most basic landlord insurance policy, providing very bare bones coverage. The DP3 is the most extensive landlord insurance policy, providing the broadest and deepest coverage.

What is covered under DP 1?

The DP1 covers the following specific perils: Fire, lightning, explosion, wind & hail, smoke, aircraft, riot & looting, vandalism, sprinkler leakage, sinkhole collapse, volcano/lava. DP3: adds everything else to the perils covered in a DP1 unless it is specifically excluded: like earthquake and flood, in Florida.

Does homeowners insurance cover broken pipes outside?

Homeowners insurance generally covers damage due to broken pipes if their collapse is sudden and unforeseen. Water damage that occurs gradually due to a leaky or rusty pipe, however, is generally not covered.

Does homeowners insurance gives you both property and liability protection?

Homeowners insurance is a package policy. This means that it covers both damage to property and liability or legal responsibility for any injuries and property damage policyholders or their families cause to other people. This includes damage caused by household pets.

Does home insurance cover mold?

Mold coverage isn’t guaranteed by your homeowners insurance policy. Typically, mold damage is only covered if it’s related to a covered peril. Mold damage caused by flooding would need to be covered by a separate flood insurance policy.

Can I remove other structures coverage?

Removing “Other Structure” Coverage Even if you have none of these items, your provider will not allow you to delete it. They are not charging an additional premium for the protection of these items. … Most homeowners have some additional structures, even if they don’t realize they do.

Is a swimming pool Coverage A or B?

Does homeowners insurance cover pool damage? Yes. … If your pool is a permanent part of the home e.g an in-ground pool, it would be considered under coverage B, ‘other structures’, and is covered against the same types of events as your house” aka Coverage A (dwelling coverage.)

What does CGL B cover?

Coverage B: Personal And Advertising Injury Liability CGL coverage B protects you from claims of slander, libel, false arrest, and even improper eviction. In addition, it provides some coverage for improperly using copyrighted material in your business.