How do you read a closing statement

By David Edwards

A mortgage closing statement lists all of the costs and fees associated with the loan, as well as the total amount and payment schedule. A closing statement or credit agreement is provided with any type of loan, often with the application itself.

What information does a closing statement contain?

A mortgage closing statement lists all of the costs and fees associated with the loan, as well as the total amount and payment schedule. A closing statement or credit agreement is provided with any type of loan, often with the application itself.

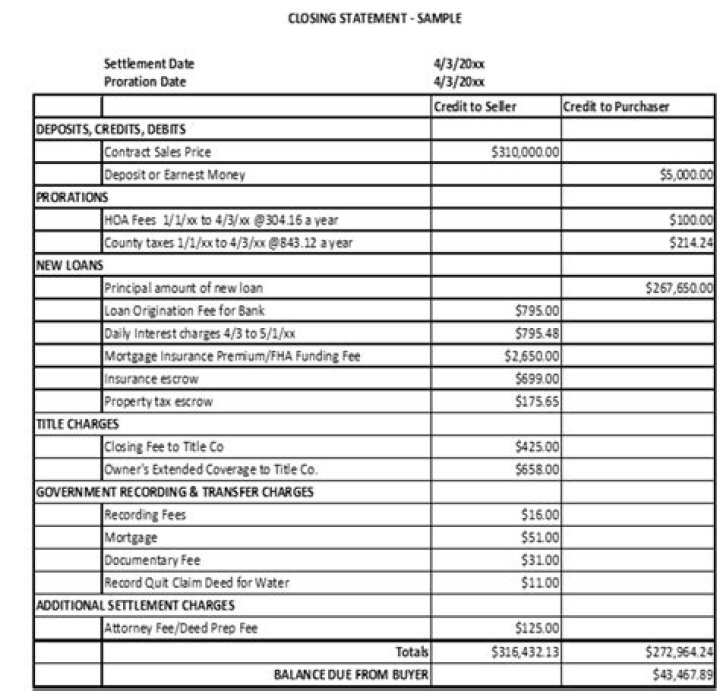

How do you read a settlement statement?

- File No./Escrow No. Think of the escrow number like a bank account number — it’s a series of digits specific to a single transaction between a buyer and seller.

- Date & Time: …

- Officer/Escrow Officer: …

- Settlement Location: …

- Property Address: …

- Buyer: …

- Seller: …

- Lender:

How do you read a sellers closing disclosure?

The Seller’s Closing Disclosure shows the purchase price and then a line item breakdown of every cost paid by the seller in two columns of whether it was paid before or at closing. (3) Totals Seller’s net proceeds (=) This identifies us as the one doing your closing. Purchase price of property.What comes after closing disclosure?

What happens after the closing disclosure? Three business days after you receive your closing disclosure, you will use a cashier’s check or wire transfer to send the settlement company any money you’re required to bring to the closing table, such as your down payment and closing costs.

What items are prorated on a closing statement?

Proration is the process of dividing various property expenses between the buyer and seller in a way that allows each party to only pay for the days he or she owns the property. There are several expenses prorated at closing, include property taxes, homeowner’s insurance, HOA dues and mortgage interest.

What does a closing statement look like in court?

Typical Closing Arguments a summary of the evidence. any reasonable inferences that can be draw from the evidence. an attack on any holes or weaknesses in the other side’s case. a summary of the law for the jury and a reminder to follow it, and.

Where do I find points on my closing disclosure?

Points are listed on your Loan Estimate and on your Closing Disclosure on page 2, Section A. By law, points listed on your Loan Estimate and on your Closing Disclosure must be connected to a discounted interest rate.What do you call a closing statement?

A closing statement, also called a HUD-1 statement or settlement sheet, is a form used in real estate transactions with an itemized list of all the costs to the buyer and seller.

Is closing Disclosure final approval?The Closing Disclosure is a final accounting of your loan’s interest rate and fees, mortgage closing costs, your monthly mortgage payment and the grand total of all payments and finance charges. The form is issued at least three days before you sign the mortgage documents.

Article first time published onWhat is a debit on the closing statement?

A debit is money you owe, and a credit is money coming to you. … On a closing statement, a debit for one side is usually balanced by a credit on the other side. For example, if a seller is credited for prepaid taxes they have already paid, there will be a debit for the buyer in the same amount.

Does a closing disclosure mean the loan is approved?

The Closing Disclosure (a.k.a. “the CD”) is the mortgage document that outlines all the details of the financing. The lender creates the initial CD after the initial underwriting approval. … The subsequent pages itemize the closing cost.

Is a settlement statement the same thing as a closing statement?

Generally, loan settlement statements can also be referred to as closing statements. Beyond just loans, settlement statements may also be used whenever a large settlement has taken place.

How is a PMM entered on a closing statement?

A new purchase money mortgage (PMM) is entered on the settlement statement as a debit to the seller and as a credit to the buyer.

How will the earnest money be shown on the closing statement?

The earnest money deposit will be listed as a credit to the buyer, while any other funds owed will be listed as debits. The closing agent will add up all of the debits and credits for the buyer to get a final amount of funds required at closing. This is the method used to apply the earnest money properly.

How do you know when your mortgage loan is approved?

How do you know when your mortgage loan is approved? Typically, your loan officer will call or email you once your loan is approved. Sometimes, your loan processor will pass along the good news.

What happens between clear to close and closing?

Clear to close means the lender is now ready to confirm the closing date with the title company or attorney. This also means you need to kick it into high gear and prepare for the closing date. Before you are clear to close, you are to meet the lender’s required conditions.

How many days before closing do you get clear to close?

Cleared to Close (3 days) Getting the all clear to close is the last step before your final loan documents can be drawn up and delivered to you for signing and notarizing.

How long should closing statement be?

Each closing argument usually lasts 20-60 minutes. Some jurisdictions limit how long the closing may be, and some jurisdictions allow some of that time to be reserved for later.

What is a good closing statement for an interview?

Finish with a polite conclusion Here are some common conclusions: “I am grateful for interviewing with you today. You have given me a clear overview of the position. I think my experience and accomplishments can provide value to the organization.

What is not prorated at closing?

Sample 2. Items Not Prorated. Seller and Buyer agree that (i) on the Closing, the Property will not be subject to any financing arranged by Seller other than the Loan; (ii) none of the insurance policies relating to the Property will be assigned to Buyer, and Buyer.

Is mortgage prorated at closing?

If your payoff date is set for a closing date in the current month, your prorated mortgage interest will be less than your monthly payment. If closing is set for the next month, your prorated mortgage interest will be more than your monthly interest payment.

Which item does a lender generally require at the closing?

Your lender is required to provide it to you at least 3 business days before your loan closing. This form lists your loan’s amount, interest rate and monthly payment, including a breakdown of how much of your payment is made up of principal, interest, private mortgage insurance, property taxes and homeowners insurance.

What is closing document?

A Closing Disclosure outlines all the terms of your loan, so you know exactly what you’re getting when you sign your mortgage. … Buyers should take the time to thoroughly review these documents to understand the details of the loan terms, conditions, payments and funds required to close.

How much is 25 points on a mortgage?

25 percentage point reduction in the interest rate and costs $1,000.

How much does 1 point lower your interest rate?

Each point typically lowers the rate by 0.25 percent, so one point would lower a mortgage rate of 4 percent to 3.75 percent for the life of the loan.

How many days after closing is disclosure?

According to the Consumer Financial Protection Bureau’s final rule, the creditor must deliver the Closing Disclosure to the consumer at least three business days prior to the date of consummation of the transaction.

Do lenders check bank statements before closing?

Do lenders look at bank statements before closing? Lenders typically will not re–check your bank statements right before closing. They’re only required when you initially apply and go through underwriting.

Do lenders verify employment after closing?

Typically, lenders will verify your employment yet again on the day of the closing. It’s kind of a checks and balances system. … In addition to your employment, your lender may also pull your credit one last time, again, to make sure nothing changed.

Can a loan be denied after closing disclosure?

Though it’s rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. … During this time frame, borrowers have the right to back out of the loan, so the bank may hold off on wiring the money right away.

Is earnest money a credit or debit at closing?

An earnest deposit or earnest money is a deposit made to a seller representing a buyer’s good faith to buy a home. At closing, buyers will be credited for this in the form of a credit. … The seller would be credited while the buyer would be debited.