What is COSO Internal Control Integrated Framework

By Olivia Bennett

COSO’s Internal Control—Integrated Framework (Framework) enables organizations to effectively and efficiently develop systems of internal control that adapt to changing business and operating environments, mitigate risks to acceptable levels, and support sound decision making and governance of the organization.

What is the COSO framework on internal control and what are the components?

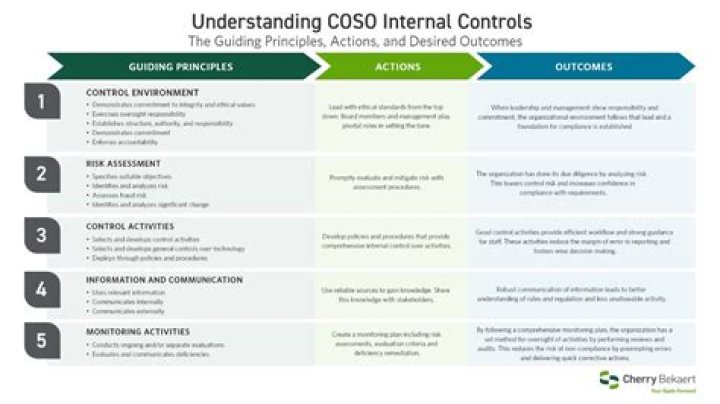

The framework that deals with internal controls are the COSO framework which consists of five components; control environment, risk assessment, control activities, information and communication, and monitoring.

Why is the COSO internal control framework necessary?

Benefit #1: Improved internal controls According to the COSO board, the updated framework offers companies more effective internal controls, which will allow organizations to better mitigate risks and have the data necessary to support sound decision-making.

What is COSO and why is it important?

The Committee of Sponsoring Organizations’ (COSO) mission is to help organizations improve performance by developing thought leadership that enhances internal control, risk management, governance and fraud deterrence.What are the COSO framework objectives?

The ultimate goal of the COSO Framework is to provide assurance that objectives have been achieved in the critical areas of operations, reporting, and compliance. The COSO framework objectives are divided into three distinct disciplines: operations, reporting, and compliance.

What is internal control framework?

An internal control framework is a structured guide that organizes and categorizes expected controls or control topics. … When an organization uses a control framework effectively (typically in audit risk assessments and risk management), management designs internal control processes with the framework as a baseline.

How do you use the COSO framework?

- PHASE 1: PLAN AND SCOPE. Appoint an implementation team. …

- PHASE 2: ASSESS AND DOCUMENT. In this phase, the implementation team assesses the organization’s control structure. …

- PHASE 3: REMEDIATE. …

- PHASE 4: DESIGN, TEST, AND REPORT. …

- PHASE 5: OPTIMIZE INTERNAL CONTROLS’ EFFECTIVENESS.

What are the benefits of an internal control framework?

Internal controls are vital to any company or organization. They ensure compliance with regulations and laws and prevent companies from fraud or theft from within. A present and functioning internal control process offers “reasonable assurance” regarding the amounts presented in an organization’s financial statements.What does Coso mean?

AcronymDefinitionCOSOCommittee of Sponsoring Organizations (est. 1985)COSOCommittee of Sponsoring Organizations of the Treadway CommissionCOSOCorporate SouthCOSOChurch of Spiral Oak

What are the COSO framework limitations?Additional Limitations of the COSO Framework COSO admits that even with a well-designed internal control system, internal auditors cannot always uncover risks of human error, poor judgment, management overrides, or employees colluding to circumvent internal control.

Article first time published onWho uses the COSO framework?

The course is offered only through COSO’s five sponsoring organizations: American Accounting Association (AAA), American Institute of Certified Public Accountants (AICPA), Financial Executives International (FEI), IMA (Institute of Management Accountants), and The Institute of Internal Auditors (IIA).

What is COSO testing?

What is COSO? COSO is the acronym used to refer to a model used for testing and evaluating internal control and processes. … This initiative has come to be known as COSO, and provides a definition and insights into best practices for a brand’s operations.

Is Coso a standard?

This model has been adopted as the generally accepted framework for internal control and is widely recognized as the definitive standard against which organizations measure the effectiveness of their systems of internal control. WHAT IS THE COSO FRAMEWORK?

What is internal control process?

Internal control is a process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance: That information is reliable, accurate and timely. Of compliance with applicable laws, regulations, contracts, policies and procedures.

What are the 5 components of COSO framework?

The five components of COSO – control environment, risk assessment, information and communication, monitoring activities, and existing control activities – are often referred to by the acronym C.R.I.M.E. To get the most out of your SOC 1 compliance, you need to understand what each of these components includes.

What is COSO in internal audit?

The COSO Framework defines an internal control system as “a process, effected by an entity’s board of directors, management, and other personnel, designed to provide reasonable assurance regarding the achievement of objectives relating to operations, reporting, and compliance.”

What is the difference between SOX and COSO?

COSO and SOX address the need for more robust internal controls from different angles. COSO provides a framework for managers to use when designing their control environment. … On the other hand, the SOX Act does not provide any guidance related to internal controls.

What is COSO risk framework?

The COSO ERM framework is one of two widely accepted risk management standards organizations use to help manage risks in an increasingly turbulent, unpredictable business landscape. … The initial mission of COSO was to study financial reporting and develop recommendations to prevent fraud.

What are the main objectives of internal control?

The primary purpose of internal controls is to help safeguard an organization and further its objectives. Internal controls function to minimize risks and protect assets, ensure accuracy of records, promote operational efficiency, and encourage adherence to policies, rules, regulations, and laws.

What are the four basic purposes of internal controls?

What are the 4 basic purposes of internal controls? safeguarding assets, Financial statement reliability, operational effieciency and compliance with management’s directives.

What are the five main objectives of internal control?

- Efficient conduct of business: …

- Safeguarding assets: …

- Preventing and detecting fraud and other unlawful acts: …

- Completeness and accuracy of financial records: …

- Timely preparation of financial statements: …

- Figure 1: Categories of controls.